The owner of an annuity receives a fixed payment every year, generally for the rest of their life. Most annuities are deferred, meaning the payout doesn’t occur until a later date. However, you can receive immediate payouts if you purchase a Medicaid-Compliant Annuity (MCA). When you buy a Medicaid annuity, you give a company a lump sum of cash in exchange for a guaranteed income stream. While only private insurance companies can issue annuities, you may purchase them through banks, financial planners, insurance agents, and brokerage firms.

The Benefits of a Medicaid Annuity

In what circumstances is a Medicaid annuity beneficial? Many Medicaid applicants are denied coverage for long-term care because they have too much money or too many assets. However, Medicaid applicants applying with insufficient funds to pay their nursing home bills can leave a healthy spouse destitute in the short term if paying out of pocket. A Medicaid-compliant annuity can accelerate eligibility for the joint state and federal Medicaid health insurance program, which pays for a person’s medical bills and nursing home care while providing reliable income for the healthy at-home spouse.

To properly plan for a Medicaid-compliant annuity, seek the advice of an elder law attorney who understands your state’s Medicaid rules. There are ordinary immediate payout annuities that are not Medicaid-compliant, so it is critical to receive the correct advice before your purchase. The goal for married couples is for the healthy spouse (the annuity owner) to collect the annuity income while the spouse needing medical benefits from Medicaid-funded extended care and nursing home benefits remains eligible.

Medicaid-Compliant Annuity Requirements

- The MCA is for an individual and must be non-assignable and irrevocable

- The annuity income payout must be based on the life expectancy table equivalent to the Social Security life expectancy tables Medicaid uses

- The annuity terms can’t extend beyond the annuity owner’s life expectancy

- All premiums will return to the client by the end of their life expectancy

- The immediate irrevocable annuity must not have a cash value

- The restricted annuity may not have balloon payments, and the distribution of annuity payments to the owner must be equal and actuarially sound

- The Medicaid beneficiary structure must comply with the state’s Medicaid recovery rules

- Guidelines and recovery rules vary by state law, often asking the State Medicaid Agency to be named as beneficiary

Drawbacks for Medicaid-Compliant Annuities

These Medicaid-compliant annuities are challenging to set up, may not cover all of your assets, and preclude you from accessing them if you require them for future needs. However, because of long-term care’s prohibitive costs, many married couples are willing to accept these potential risks because Medicare does not cover long-term care. The national average for long-term care insurance for a couple both 60 years old is $3,400, and approximately 30 percent of applicants between 60 and 69 are declined coverage.

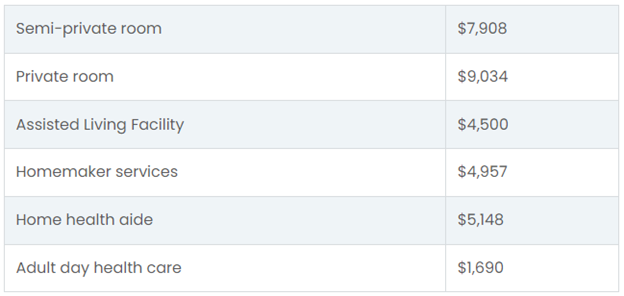

While that may seem like a lot of money to pay in premiums, if you qualify for the insurance, it pales in comparison to the national estimates of long-term care costs out of pocket. According to Genworth, the cost of long-term care in a 2021 survey cites the following monthly average costs:

Non-Countable Income Stream

Purchasing a Medicaid annuity converts an asset into a monthly income stream for the healthy spouse, and this income does not count toward Medicaid eligibility. Purchasing this annuity type means the couple’s assets do not have to be “spent down” for one to be Medicaid eligible. However, the annuity payments must be completed before the end of the healthy spouse’s life expectancy so that the annuity purchase does not become giftable to heirs.

A Medicaid-compliant annuity will convert liquid assets into a lifelong income stream that helps a healthy spouse maintain their quality of life while the spouse in need of long-term care can still qualify for Medicaid. The Medicaid-friendly annuity requires that it be irrevocable (unchangeable) and non-transferrable to heirs upon your death. Since this purchase must be irrevocable to achieve the goals, it is crucial to meet with an elder law attorney to ensure your selection is the right financial product for your circumstances. A Medicaid-compliant annuity can help both spouses in a marriage to get the resources they need should one require long-term care.

For assistance, contact us today at 312-878-0155 to speak with experienced elder law attorneys who specialize in long-term care and Medicaid.